Page 205 - 香港房屋協會 Hong Kong Housing Society Annual Report 2020/2021

P. 205

香港房屋協會 2020/21 年度年報

203

AUDITED FINANCIAL STATEMENTS 已審核財務報表 NOTES TO THE FINANCIAL STATEMENTS 財務報表附註

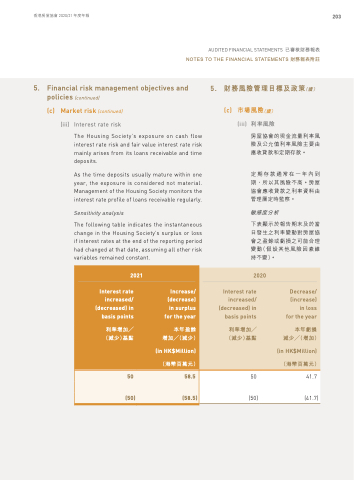

5. Financial risk management objectives and policies (continued)

(c) Market risk (continued) (iii) Interest rate risk

The Housing Society’s exposure on cash flow interest rate risk and fair value interest rate risk mainly arises from its loans receivable and time deposits.

As the time deposits usually mature within one year, the exposure is considered not material. Management of the Housing Society monitors the interest rate profile of loans receivable regularly.

Sensitivity analysis

The following table indicates the instantaneous change in the Housing Society’s surplus or loss if interest rates at the end of the reporting period had changed at that date, assuming all other risk variables remained constant.

5. 財務風險管理目標及政策(續) (c) 市場風險(續)

(iii) 利率風險

房屋協會的現金流量利率風 險及公允值利率風險主要由 應收貸款和定期存款。

定期存款通常在一年內到 期,所以其風險不高。房屋 協會應收貸款之利率資料由 管理層定時監察。

敏感度分析

下表顯示於報告期末及於當 日發生之利率變動對房屋協 會之盈餘或虧損之可能合理 變動(假設其他風險因素維 持不變)。

2021

2020

Interest rate increased/ (decreased) in basis points

Increase/ (decrease) in surplus for the year

Interest rate increased/ (decreased) in basis points

Decrease/ (increase) in loss for the year

利率增加╱ (減少)基點

本年盈餘 增加╱(減少)

利率增加╱ (減少)基點

本年虧損 減少╱(增加)

(in HK$Million)

(in HK$Million)

(港幣百萬元)

(港幣百萬元)

50

58.5

50

41.7

(50)

(58.5)

(50)

(41.7)