137 / 166

137 / 166

5

財務風險管理目標及政策

(續)

(d)

金融資產及負債按公允價值

計量

(續)

公允價值等級

(續)

—

第二級估值:使用第二級輸

入數據計量其公允價值,即

未能符合第一級之可觀察輸

入數據及不使用重大不可觀

察輸入數據。不可觀察輸入

數據仍市場數據未能提供之

輸入數據。

—

第三級估值:以輸入重大不

可觀察數據以計量公允價值。

5 Financial risk management objectives and

policies

(continued)

(d) Financial assets and liabilities measured at

fair value

(continued)

Fair value hierarchy

(continued)

—

Level 2 valuations: Fair value measured using Level 2

inputs, i.e. observable inputs which fail to meet Level 1,

and not using significant unobservable inputs.

Unobservable inputs are inputs for which market data are

not available.

—

Level 3 valuations: Fair value measured using significant

unobservable inputs.

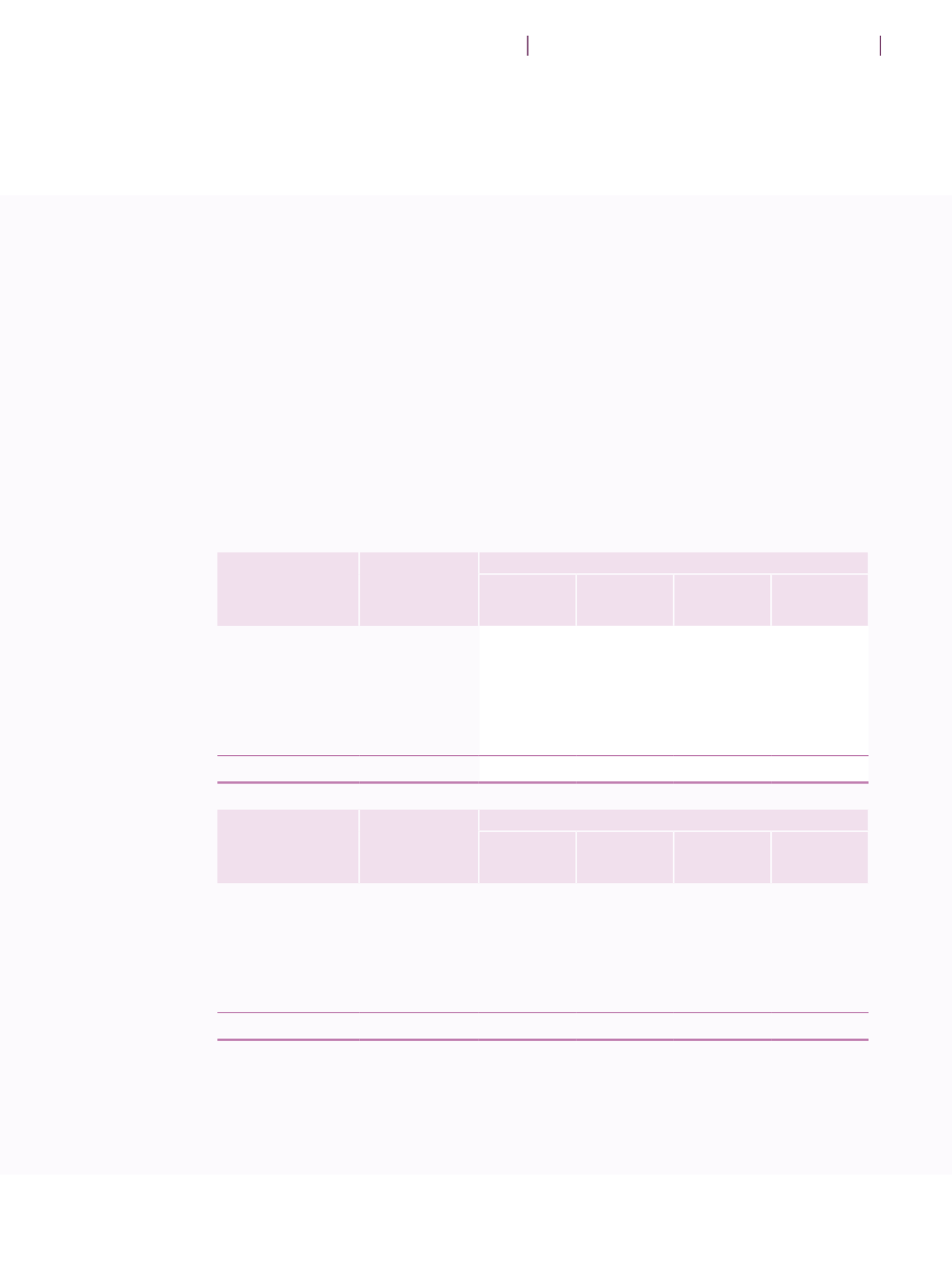

2016

Recurring fair value

measurement

(in HK$Million)

經常性公允

價值計量

(港幣百萬元)

Level 1

第一級

Level 2

第二級

Level 3

第三級

Total

總額

Investment related

financial assets

(note 16)

有關投資的

財務資產

(註十六)

7,367.8

6,404.1

1,247.6 15,019.5

Investment related

financial liabilities

(note 16)

有關投資的

財務負債

(註十六)

(3.1)

(90.2)

–

(93.3)

7,364.7

6,313.9

1,247.6 14,926.2

2015

Recurring fair value

measurement

(in HK$Million)

經常性公允

價值計量

(港幣百萬元)

Level 1

第一級

Level 2

第二級

Level 3

第三級

Total

總額

Investment related

financial assets

(note 16)

有關投資的

財務資產

(註十六)

7,929.7

6,294.3

492.6

14,716.6

Investment related

financial liabilities

(note 16)

有關投資的

財務負債

(註十六)

(3.4)

(66.7)

–

(70.1)

7,926.3

6,227.6

492.6

14,646.5

133

香港房屋協會

2016

年年報

Notes to the Financial Statements

財務報表附註